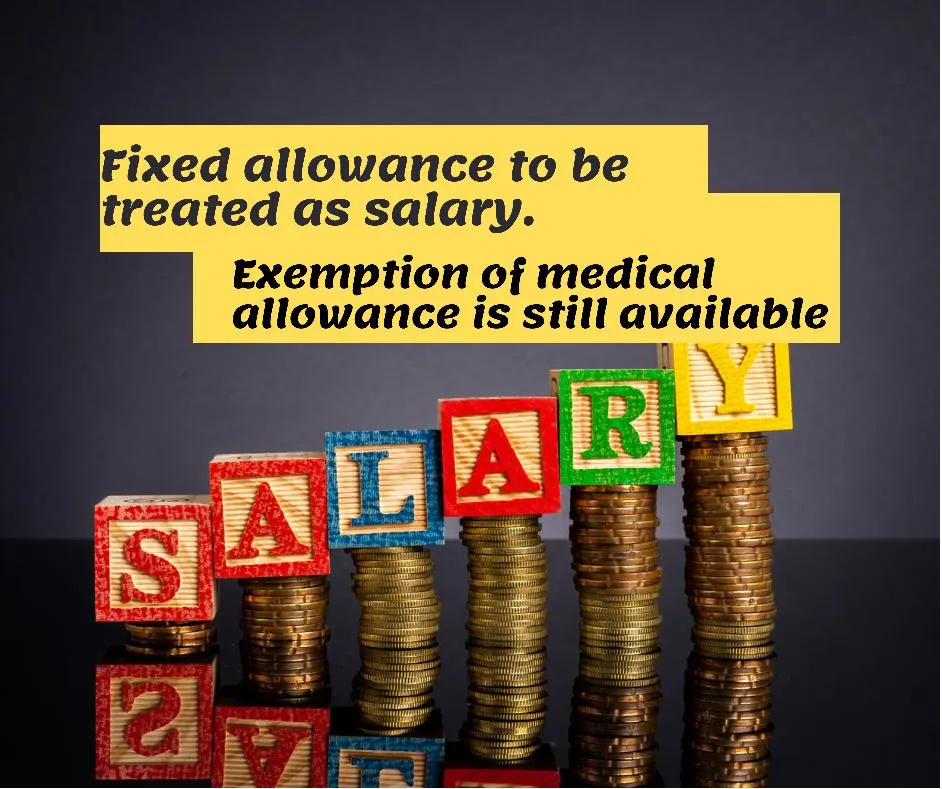

Amendments in Finance Act 2021 regarding Salary Income

“Provisions of clause (c) of sub-section (2) of section 12 were prone to misuse regarding the exemption available to allowance solely expended in the performance of employee’s duty in

conjunction with clause (39) of Part I of second schedule. The provisions were used to avoid tax. In order to streamline, an explanation has been inserted in clause (c) of sub-section (2) of

section 12 whereby the exempt allowance has been explained and consequently clause (39) of Part I of second schedule has been omitted. Any allowance which is paid on fixed basis or

percentage of salary basis shall not constitute allowance for the performance of duties.”

Explanation of Changes in Salary Income as per Finance Act 2021

Salary – Explained “allowance solely expended in the performance of employee’s duty” [Section 12]

Common components of salary are available in Section 12(2) of the Income Tax Ordinance, 2001. Clause (c) provides:

“the amount of any allowance provided by an employer to an employee including a cost of living, subsistence, rent, utilities, education, entertainment or travel allowance, but shall not include any allowance solely expended in the performance of the employee’s duties of employment;”

The Section 12 of the Income Tax Ordinance, 2001 is read as:

Salary.—(1) Any salary received by an employee in a tax year, other than salary that is exempt from tax under this Ordinance, shall be chargeable to tax in that year under the head “Salary”.

(2) Salary means any amount received by an employee from any employment, whether of a revenue or capital nature, including —

(a) any pay, wages or other remuneration provided to an employee, including leave pay, payment in lieu of leave, overtime payment, bonus, commission, fees, gratuity or work condition supplements (such as for unpleasant or dangerous working conditions);

(b) any perquisite, whether convertible to money or not;

(c) the amount of any allowance provided by an employer to an employee including a cost of living, subsistence, rent, utilities, education, entertainment or travel allowance, but shall not include any allowance solely expended in the performance of the employee’s duties of employment;

As the allowance solely expended in the performance of the employee’s duties of employment are excluded from the definition of salary, generally people misuse the provision and exclude certain amounts from taxable salary. Therefore, the Act inserted following explanation in clause (c) to provide more clarity:

Explanation.– “For removal of doubt, it is clarified that the allowance solely expended in the performance of employee’s duty does not include – (i) allowance which is paid in monthly salary on fixed basis or percentage of salary; or (ii) allowance which is not wholly, exclusively, necessarily or actually spent on behalf of the employer.“

Exemption available in Clause (39), Part I, Second Schedule also withdrawn

Further, a similar exemption available in Clause (39), Part I, Second Schedule is also withdrawn. Omitted clause is reproduced below for ready reference of the readers:

“Any special allowance or benefit (not being entertainment or conveyance allowance) or other perquisite within the meaning of section 12 specially granted to meet expenses wholly and necessarily incurred in the performance of the duties of an office or employment of profit”.

Exemption of 10 (%) percent Medical allowance and other medical facility is still available

Through Finance Bill 2021, Clause (139), Part I, Second Schedule which provides exemption of medical allowance and medical facility provided by the employer to an employee was proposed to be removed. However, the parliament did not approve such omission, so the exemption under clause (139), Part I, Second Schedule relevant to medial allowance and other medical facility is still intact and available to the employees.

Salary Income | Salary Allowance | Taxable Salary Income | Fixed Allowance | Percentage of Salary | Medical allowance |