A person who wants to become an informer, he should get himself first register with FBR for this purpose. Then he will able to get reward for the sharing of information with the Federal Board of Revenue (FBR).

Complete procedure for registration as informer and other conditions are specified in the Income Tax Rules, 2002.

Informer means

An “Informer” means any person, a group of persons or a company who provides any original information in the shape of concrete evidence, which conclusively leads to detection of tax evasion, formulation of assessment, and eventual recovery of the evaded tax and includes a whistleblower as defined under the tax laws;

Informer Definition | Income Tax Rules 2002 |

Persons qualified to be registered as informer

Persons qualified to be registered as informer. (1) A person, other than a lunatic or idiot, may be registered as informer, if he fulfills the criteria of whistleblower as defined in the tax laws.

Persons Qualified to be registered as informer | Income Tax Rules 2002 |

(2) Notwithstanding anything contained in sub-rule (1), a registered informer shall be liable to de-registration on such condition to be recorded in writing and as may be deemed fit by Chief Commissioner, member or Director General, as the case may be.

Registration of informer

Registration of informer. A person desirous of getting himself registered as an informer may make an application to the Chief Commissioner for registration under this rule.

Registration of Informer | Income Tax Rules 2002 |

The application shall be in the prescribed form and shall be verified in the prescribed manner.

(3) The application shall be accompanied by the following documents, namely.-

(a) copy of the Computerized National Identity Card of the applicant;

(b) copy of national tax number (NTN) certificate; and

(c) a duly sworn in affidavit stating therein that the correct information provided and nothing concealed there from and that in case any incorrect information provided or any information concealed he will liable to penal action under the laws.

Submission of information and further action thereupon

Submission of information and further action thereupon.-(1) An informer shall submit any information regarding concealment or evasion of tax leading to detection or collection of taxes, fraud, corruption or misconduct that is in his possession to the Chief Commissioner giving precise details of the alleged act along with all supporting evidences that are in his possession:

The information is accompanied with the supporting evidences.

(2) On receipt of the information, the Chief Commissioner shall scrutinize the information and forward it to the concerned Commissioner.

(3) On receipt of the information from the Chief Commissioner, the concerned Commissioner shall conduct such further inquiry as he may deem fit and submit his report to the Chief Commissioner.(4) On completion of the inquiry, the concerned Commissioner shall take such further action as required under the tax laws or any other law for the time being in force, as may be necessary on the basis of the facts of the case, and furnish his report to the Chief Commissioner.

Submission of information by informer | Income Tax Rules 2002 |

(5) Notwithstanding anything contained in these rules, an informer, who −

(a) has knowingly provided false information under these rules; or

(b) has provided the information under these rules with the intention to intimidate or blackmail a person, or to bring him into disrepute, or to otherwise cause him financial loss, shall be liable to punishment and fine under the tax laws and other laws for the time being in force.

Eligibility for reward

An employee and an informer will be entitled to a grant of reward for their conduct.

Determination of reward

| Amount of tax evaded | Amount of reward |

| 1 | 2 |

| Rs. 500,000 or less | Twenty per cent of the tax, duty and other taxes |

| More than Rs. 500,00 but not more than 1,000,000 | Rs. 100,000 plus ten percent of the tax in excess of Rs. 500,000 |

| Over Rs. 1,000,000 | Rs. 150,000 plus five per cent of the tax in excess of Rs. 1,000,000 |

Sanctioned of the reward shall be after realization of the whole amount of the tax involved. Provided that the total amount of reward paid to an “employee” during one financial year shall not exceed thirty six months’ basic pay. In case an employee performs more than one meritorious conduct, the amount of reward shall not exceed thirty percent of realization of the whole amount of tax involved.

FBR | Federal Board of Revenue | Whistle-blower | Tax Evasion | FBR Informer |

LATEST POSTS

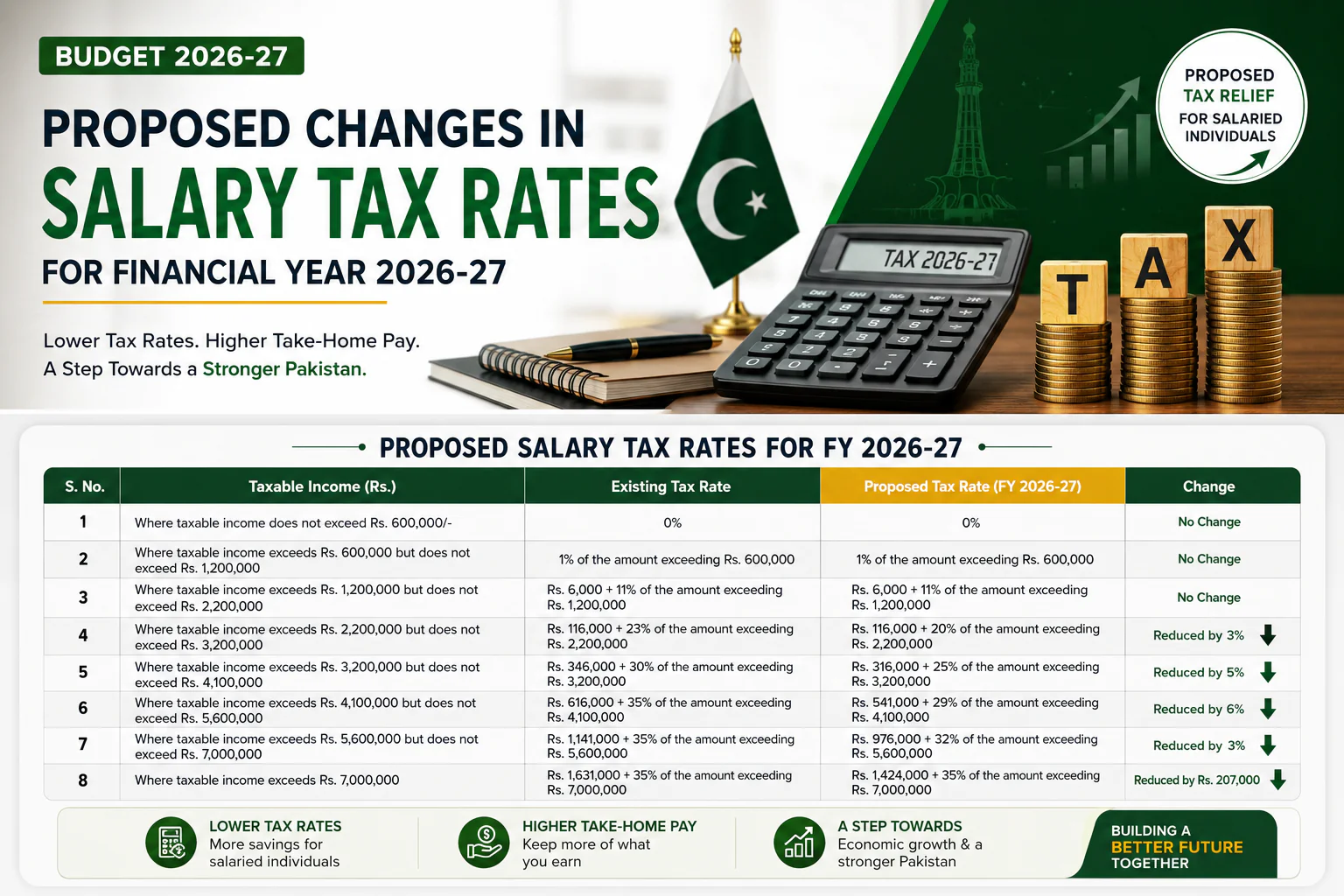

- Pakistan Budget 2026-27: Proposed Salary Tax Rates for Salaried Individuals

Proposed Salary Tax Rates for Salaried Individuals in Pakistan Budget 2026-27 The Finance Bill for the 2026‑27 budget proposes a reduction in income tax rates for salaried individuals. Most salaried taxpayers above Rs. 2.2 million in annual taxable income will enjoy a reduction in their tax liability. Here is the proposed slabs, existing salary tax rates, and how much salaried individuals can save once the changes in tax rates take effect. Proposed vs. Existing Salary Tax Rates for FY 2026‑27 S.No Taxable Income Existing Tax Rate Proposed Tax Rate 1 Up to Rs. 600,000 0% 0% 2 Rs. 600,000 – Rs. 1,200,000 1% of amount exceeding Rs. 600,000 1% of amount exceeding Rs. 600,000 3 Rs. 1,200,000 – Rs. 2,200,000 Rs. 6,000 + 11% of amount exceeding Rs. 1,200,000 Rs. 6,000 + 11% of amount exceeding Rs. 1,200,000 4 Rs. 2,200,000 – Rs. 3,200,000 Rs. 116,000 + 23% of amount exceeding Rs. 2,200,000 Rs. 116,000 + 20% of amount exceeding Rs. 2,200,000 5 Rs. 3,200,000 – Rs. 4,100,000 Rs. 346,000 + 30% of amount exceeding Rs. 3,200,000 Rs. 316,000 + 25% of amount exceeding Rs. 3,200,000 6 Rs. 4,100,000 – Rs. 5,600,000 Rs. 616,000 + 35% of amount exceeding Rs. 4,100,000 Rs. 541,000 + 29% of amount exceeding Rs. 4,100,000 7 Rs. 5,600,000 – Rs. 7,000,000 Rs. 1,141,000 + 35% of amount exceeding Rs. 5,600,000 Rs. 976,000 + 32% of amount exceeding Rs. 5,600,000 8 Above Rs. 7,000,000 Rs. 1,631,000 + 35% of amount exceeding Rs. 7,000,000 Rs. 1,424,000 + 35% of amount exceeding Rs. 7,000,000 Who Benefits the Most From the Proposed Salary Tax Slabs? The first two taxable slabs (income up to Rs. 2.2 million) are unchanged, means initial salaried tax slabs won’t see any difference. The change starts from slab 4 onward up to slab no 7. How to Calculate Your Tax Under the New Slabs To calculate your annual tax liability of salary income, you have to identify which slab your taxable salary income falls into. Then apply the formula for that slab: the fixed amount of salary tax plus the stated percentage of salary tax rate of that slab multiply by the income exceeding the slab’s lower threshold. For example, someone earning Rs. 4,500,000 falls in slab 6: Rs. 541,000 + 29% of (Rs. 4,500,000 − Rs. 4,100,000) = Rs. 541,000 + Rs. 116,000 = Rs. 657,000. Additional Tax Surcharge Removed Government of Pakistan has also proposed in the budget 2026-2027 removal of tax surcharge @9% on salary income if it is above than Rs 10 Million Rupees per annum. It is in addition to salary tax rates reductions proposed in the budget. FAQs Section TAGS A step-by-step guide to filing an income tax return | How to compute monthly withholding tax from salary | Budget 2026-27 | Salary Tax Slabs | Income Tax Rates | Finance Bill 2026-27 | Tax Calculator | Salaried Individuals Tax | Income Tax Ordinance | FBR Tax Slabs | Tax Relief | Withholding Tax | Salary Tax Rates 2026-27 | New Tax Slabs Pakistan | Income Tax Calculation Guide | Budget Tax Changes |

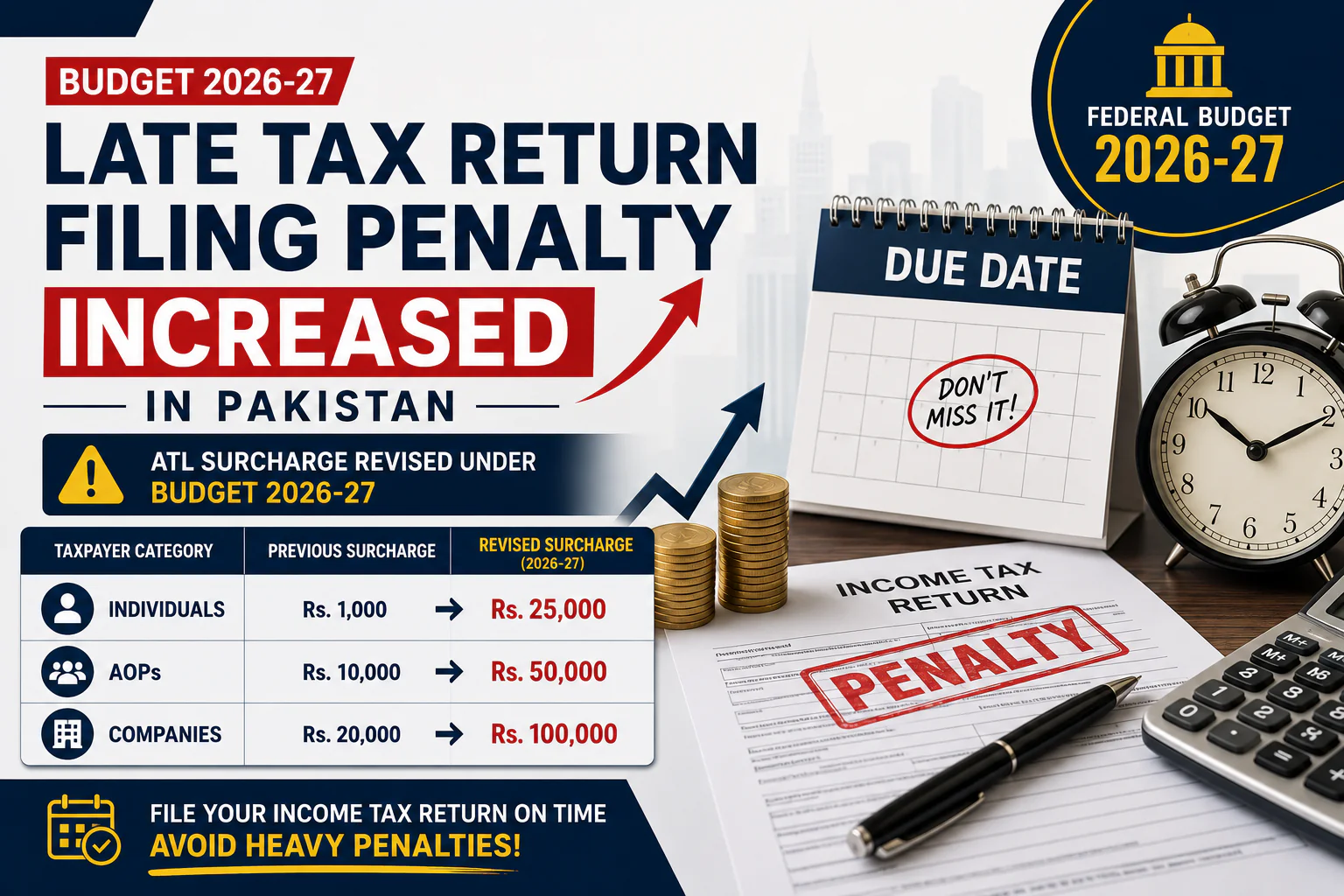

Proposed Salary Tax Rates for Salaried Individuals in Pakistan Budget 2026-27 The Finance Bill for the 2026‑27 budget proposes a reduction in income tax rates for salaried individuals. Most salaried taxpayers above Rs. 2.2 million in annual taxable income will enjoy a reduction in their tax liability. Here is the proposed slabs, existing salary tax rates, and how much salaried individuals can save once the changes in tax rates take effect. Proposed vs. Existing Salary Tax Rates for FY 2026‑27 S.No Taxable Income Existing Tax Rate Proposed Tax Rate 1 Up to Rs. 600,000 0% 0% 2 Rs. 600,000 – Rs. 1,200,000 1% of amount exceeding Rs. 600,000 1% of amount exceeding Rs. 600,000 3 Rs. 1,200,000 – Rs. 2,200,000 Rs. 6,000 + 11% of amount exceeding Rs. 1,200,000 Rs. 6,000 + 11% of amount exceeding Rs. 1,200,000 4 Rs. 2,200,000 – Rs. 3,200,000 Rs. 116,000 + 23% of amount exceeding Rs. 2,200,000 Rs. 116,000 + 20% of amount exceeding Rs. 2,200,000 5 Rs. 3,200,000 – Rs. 4,100,000 Rs. 346,000 + 30% of amount exceeding Rs. 3,200,000 Rs. 316,000 + 25% of amount exceeding Rs. 3,200,000 6 Rs. 4,100,000 – Rs. 5,600,000 Rs. 616,000 + 35% of amount exceeding Rs. 4,100,000 Rs. 541,000 + 29% of amount exceeding Rs. 4,100,000 7 Rs. 5,600,000 – Rs. 7,000,000 Rs. 1,141,000 + 35% of amount exceeding Rs. 5,600,000 Rs. 976,000 + 32% of amount exceeding Rs. 5,600,000 8 Above Rs. 7,000,000 Rs. 1,631,000 + 35% of amount exceeding Rs. 7,000,000 Rs. 1,424,000 + 35% of amount exceeding Rs. 7,000,000 Who Benefits the Most From the Proposed Salary Tax Slabs? The first two taxable slabs (income up to Rs. 2.2 million) are unchanged, means initial salaried tax slabs won’t see any difference. The change starts from slab 4 onward up to slab no 7. How to Calculate Your Tax Under the New Slabs To calculate your annual tax liability of salary income, you have to identify which slab your taxable salary income falls into. Then apply the formula for that slab: the fixed amount of salary tax plus the stated percentage of salary tax rate of that slab multiply by the income exceeding the slab’s lower threshold. For example, someone earning Rs. 4,500,000 falls in slab 6: Rs. 541,000 + 29% of (Rs. 4,500,000 − Rs. 4,100,000) = Rs. 541,000 + Rs. 116,000 = Rs. 657,000. Additional Tax Surcharge Removed Government of Pakistan has also proposed in the budget 2026-2027 removal of tax surcharge @9% on salary income if it is above than Rs 10 Million Rupees per annum. It is in addition to salary tax rates reductions proposed in the budget. FAQs Section TAGS A step-by-step guide to filing an income tax return | How to compute monthly withholding tax from salary | Budget 2026-27 | Salary Tax Slabs | Income Tax Rates | Finance Bill 2026-27 | Tax Calculator | Salaried Individuals Tax | Income Tax Ordinance | FBR Tax Slabs | Tax Relief | Withholding Tax | Salary Tax Rates 2026-27 | New Tax Slabs Pakistan | Income Tax Calculation Guide | Budget Tax Changes | - Budget 2026-27: Government Proposes Massive Increase in Late Tax Return Filing PenaltiesLate Tax Return Filing Penalty Increased in Pakistan Under Budget 2026-27 The Federal Budget 2026–27 has proposed a major increase in the late tax return filing penalties (ATL surcharge) imposed on taxpayers (individuals, AOPs and Companies) who file their income tax returns after the due date. Through an amendment to Section 182A(1)(a) of the Income Tax Ordinance, 2001, the Federal Government has revised the ATL (Active Taxpayers List) surcharge as follows: Taxpayer Category Previous Surcharge Proposed Surcharge Individuals Rs. 1,000 Rs. 25,000 AOPs Rs. 10,000 Rs. 50,000 Companies Rs. 20,000 Rs. 100,000 The proposed amendment is to encourage timely filing of income tax returns and increase tax compliance across the country. The increase is particularly significant for individuals, where the surcharge raised twenty-five times from Rs. 1,000 to Rs. 25,000. Similarly, companies may face a surcharge of Rs. 100,000 for late filing, compared to the previous amount of Rs. 20,000. Now, taxpayers are advised to file their annual income tax returns within the prescribed due dates to avoid heavy penalties and maintain their status on the Active Taxpayers List (ATL) with FBR. How to File Income Tax Return in Pakistan | Benefits of Being an Active Taxpayer | ATL Status Check Online | FBR Iris Registration Guide | Income Tax Return Due Dates in Pakistan | Penalties for Non-Filers in Pakistan | Budget 2026-27 Highlights | Income Tax Rates in Pakistan 2026

- Pakistan Budget 2026-27 to Be Presented Today in National AssemblyPakistan Budget 2026-27 to Be Announced Today Islamabad, June 12, 2026: The Federal Government is scheduled to present the Pakistan Budget 2026-27 in the National Assembly today. Finance Minister Muhammad Aurangzeb will present the federal budget proposals for the upcoming fiscal year 2026-2027. He will unveil it after approval by the Federal Cabinet. The National Assembly session for the budget presentation is expected to begin at 3:00 PM. The budget is expected on the government’s revenue targets, expenditure plans, taxation measures, and key economic priorities for FY 2026-27. Businesses, taxpayers, investors, and salaried individuals all over the Pakistan are keenly watching today’s budget announcement for any changes in taxes, salaries, pensions, and other fiscal measures. Tax.net.pk will provide live updates, budget highlights, and detailed analysis immediately after the budget speech. Tags Federal Budget Pakistan | Income Tax Rates in Pakistan | FBR Tax Updates | Salary Tax Calculator Pakistan | Withholding Tax Rates in Pakistan | Prize Bond Draw Schedule 2026 | Petrol Prices in Pakistan | Pakistan Economic Updates | Tax News Pakistan | Budget 2026-27 Highlights

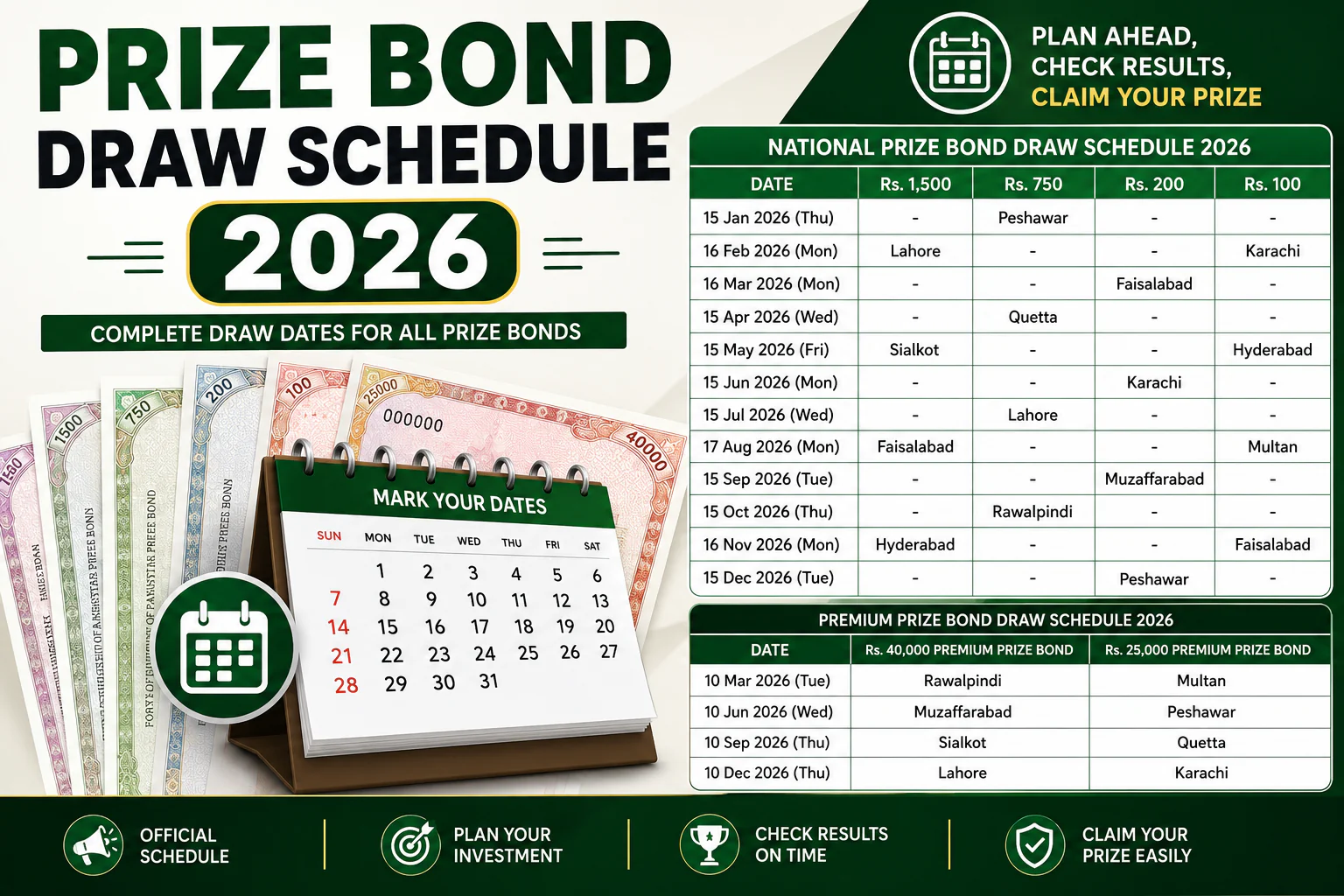

- Prize Bond Draw Schedule 2026 Pakistan – Complete Draw Dates ListPrize Bond Draw Schedule 2026 In Pakistan, prize bonds is very popular investment among the people. People like to invest in this mode of investment because it’s easy to invest, encash, backed by the Government of Pakistan, and profit is also paid on the premium prize bonds. Knowing prize bonds draw dates in advance is very important because you never miss a draw result, stay updated with official announcements, easy to manage, and timely prize money process, peace of mind. Here schedule for the year starting from January 2026 to December 2026 is given. Such schedule is for denominations of: Prize bond schedule for 2026 is also given here for premium prize bonds of: Prize Bond Draw Schedule 2026 Here prize bond draw schedule for 2026 is given for regular type of prize bonds which is not issued in name of investor. Any body can purchase it and invest easily. Schedule is for prize bonds for denominations of Rs 1500, Rs 750, Rs 200, and Rs 100. Date Rs. 1,500 Rs. 750 Rs. 200 Rs. 100 15 January 2026 (Thursday) – Peshawar – – 16 February 2026 (Monday) Lahore – – Karachi 16 March 2026 (Monday) – – Faisalabad – 15 April 2026 (Wednesday) – Quetta – – 15 May 2026 (Friday) Sialkot – – Hyderabad 15 June 2026 (Monday) – – Karachi – 15 July 2026 (Wednesday) – Lahore – – 17 August 2026 (Monday) Faisalabad – – Multan 15 September 2026 (Tuesday) – – Muzaffarabad – 15 October 2026 (Thursday) – Rawalpindi – – 16 November 2026 (Monday) Hyderabad – – Faisalabad 15 December 2026 (Tuesday) – – Peshawar – Premium Prize Bond Draw Schedule 2026 This premium prize bonds schedule is for denominations of Rs 40,000 and Rs 25,000. Draw of premium prize bonds is held quarterly. This type of prize bond is issued in the name of investor. It has benefits like, it is very secure, no risk of theft, profit on investment, and easy to manage. Draw of Premium prize bonds is held quarterly in the following months: Date Rs. 40,000 Premium Prize Bond Rs. 25,000 Premium Prize Bond 10 March 2026 (Tuesday) Rawalpindi Multan 10 June 2026 (Wednesday) Muzaffarabad Peshawar 10 September 2026 (Thursday) Sialkot Quetta 10 December 2026 (Thursday) Lahore Karachi How to Check Latest Prize Bonds Draw Result Online Prize Bond List Online check through: Call to Action If you need help with NTN registration, income tax return filing, ATL status, or FBR matters? You may please Contact Global Tax Consultants for professional tax advisory and compliance services across Pakistan. 💬 WhatsApp Chat 📞 Call Now

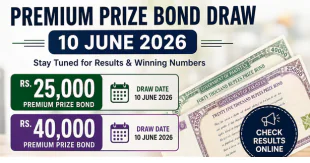

- Premium Prize Bond Draw 10 June 2026 for Rs. 25,000 and Rs. 40,000 BondsPremium Prize Bond Draw for Rs. 25,000 and Rs. 40,000 on 10 June 2026 The next Premium Prize Bond Draw for denominations of Rs. 25,000 and Rs. 40,000 is scheduled to be held on 10 June 2026. Prize bond holders across Pakistan wait for the official draw results announced by the State Bank of Pakistan (SBP) and National Savings Pakistan. Premium Prize Bonds is very popular among public because: they offer regular profit payments and opportunity to win prizes as well. What Are Premium Prize Bonds? Premium Prize Bonds are different from regular prize bonds, these bonds provide: Currently, Premium Prize Bonds are available in denominations of Rs. 25,000 and Rs. 40,000. Next Draw Date and Details Premium Prize Bond Rs. 25,000 Draw Premium Prize Bond Rs. 40,000 Draw The official winning numbers will be announced after the draw is conducted by National Savings Pakistan. How to Check Premium Prize Bond Draw Results Online Prize bond holders can check the draw results through: After the draw, winning lists will be available for online verification. Benefits of Investing in Premium Prize Bonds Premium Prize Bonds offer many benefits: Regular Profit Income Premium bond holders receive profit payments directly into their linked bank accounts. Chance to Win Prizes In addition to profit income, investors can also win prize amount on scheduled draw dates. Government-Backed Investment Premium Prize Bonds are issued by the Government of Pakistan, making them one of the reliable investment options. Easy to Maintain and No Risk of Theft Premium bonds are registered in the investor’s name, ownership records remain secure and no risk of theft. When Will the Result Be Available? The official draw result is announced after the draw will be held on 10 June 2026. Once announced, bond holders can search their bond numbers online and verify whether they have won any prize. Stay Updated If you hold Premium Prize Bonds of Rs. 25,000 or Rs. 40,000, make sure to check back on 10 June 2026 for the latest draw results, winning numbers, and prize details. We will update this page immediately after the official announcement.

- New Taxes on E-commerce Transactions in PakistanNew Taxes on E-commerce Transactions in Pakistan: In the recent budget (Finance Act 2025) Government of Pakistan has taken some significant steps towards the taxation of local ecommerce industry of Pakistan. The new amendments in the Income tax Ordinance 2001 and Sales Tax Act 1990 will affect all those ecommerce businesses operating through online platforms, websites, or courier based Cash on Delivery (COD) Model. Below are the significant highlights of amendments in tax laws of Pakistan which are necessary for your understanding: Enhanced Definition of “Online Market Place” Through Finance Act 2025, section 2(38B) of income Tax Ordinance 2001 amended and definition of “Online Market Place” has been broadened. It now also includes: These will help buying and selling between multiple parties, whether the platform owns the goods/services or not. New Taxes on E-commerce Transactions in Pakistan for Digitally Ordered Goods/Services Through Finance Act 2025, a new section, 6A in the Income Tax Ordinance, introduces a tax on payments received for digitally ordered goods/services through local platforms (including websites). Applies To:This section applies to all persons receiving payments for goods/services delivered from within Pakistan via online platforms. Excludes:It does not include export proceeds received in Pakistan which are already taxed under sections 154 and 154A. Tax Collection by Payment Intermediaries and & Couriers Under amendment in section 153(2A) of Income Tax Ordinance 2001 through Finance Act 2025: This applies to all payments made for digitally ordered goods and services via local platforms, including websites. Rate of Income tax to be deducted from a payment for digitally ordered goods/services Two different tax rates has been introduced for payments to ecommerce sellers against digitally ordered goods, complete description is here: Sales Tax Collection Responsibility As per Sales Tax Act 1990, the responsibility to collect and pay sales tax on digitally ordered goods is explained here: Rates of Sales Tax on Payments against Digitally ordered goods The applicable rates of sales tax to be deducted are given in the Eleventh Schedule of the Sales Tax Act 1990. The sales tax withheld by the payment intermediary or the courier company will be final discharge of tax liability against the digitally ordered goods by the: AS per the eleventh schedule of Sales Tax Act 1990 the rate of sales tax to withhold to withhold by the payment intermediary / Courier Company will be at the rate of 2% of gross value of supplies. Mandatory NTN & Sales Tax Registration To promote documentation and transparency: Unregistered sellers will not be allowed to operate on their platforms.

TaxUrdu.com