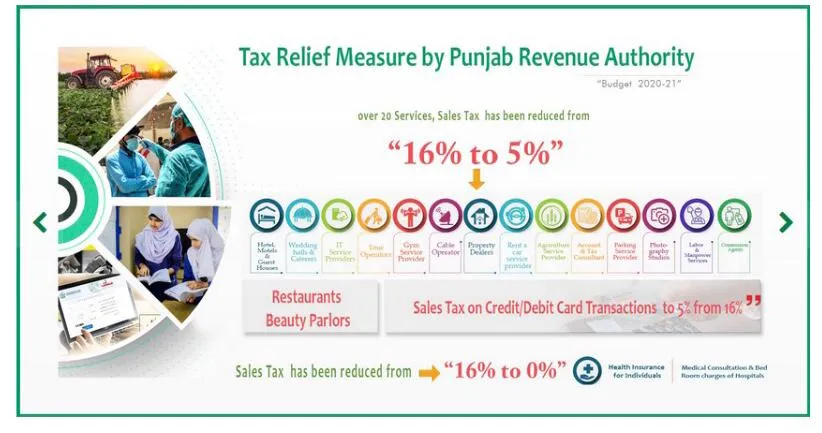

Through the Finance Act, 2020, the Government of the Punjab reduced the rate of Punjab Sales Tax on Services from 16% to 5% on more than twenty services. Punjab Revenue Authority also reduced the rate on payments made through credit / debit cards to restaurants and beauty parlours to 5%. Government also provided a big relief to Medical profession by reducing the sales tax rate to Zero Percent.

HOTELS, MOTELS, GUEST HOUSES, MARRIAGE HALLS, CLUBS CATERING SERVICES

Hotels, motels and guest houses. 9801.1000

Tax Rate: Five percent without input tax adjustment for noncorporate, nonfranchise, nonchain businesses with less than 20 rooms; and Sixteen percent for others.

Marriage halls and lawns (by whatever name called) 9801.3000 including pandal and shamiana services. Tax Rate: Five percent without input tax adjustment.

Clubs including race clubs and their membership services 9801.4000 including services, facilities or advantages, for a subscription or any other amount, to their members. Tax Rate: Sixteen percent.

Catering services (including all ancillary/allied 9801.5000 services such as floral or other decoration, furnishing of space whether or not involving rental of equipment. Tax Rate: Five percent without input tax adjustment.

RESTAURANTS

Services provided by restaurants [including cafes, food (including ice-cream) parlors, coffee houses, coffee shops, deras, food huts, eateries, resorts and similar cooked, prepared or ready-to-eat food service outlets etc 9801.2000 & 9801.9000.

Tax Rate: Five percent without input tax adjustment where payment against services is received through debit or credit cards; and Sixteen percent for others.

Franchise service relating to education services

Franchise service including intellectual property rights services and licensing services. [9823.0000, 9839.0000.

Tax Rate: Five percent without input tax adjustment for services relating to educational institutions; and Sixteen percent for others.

Construction services

Construction services and services provided by contractors of building.

Tax Rate: Five percent without input tax credit/adjustment in respect of Government civil works and sixteen percent with input tax credit/adjustment for others.

Explanation- Notwithstanding the rate of 5% fixed in column 4 of second schedule, the following further reduced rates shall be applicable:

a)- one per cent for all services specified at S.No.14 without input tax credit or adjustment to the extent of Government civil works including those of cantonment boards involved in the ongoing development schemes and projects launched during Financial Year 2016-17 and funded under the Annual Development Plan of the Punjab Government or funded through foreign loans where the negotiations were finalized after 1st of July 2016 or funded under Public Sector Development Program of the Federal Government or funded by the Cantonment Boards; and

b)- zero per cent for all services specified at S.No.14 without input tax credit/adjustment to the extent of Government civil works including those of cantonment boards involved in the ongoing development schemes and projects launched prior to Financial Year 2016-17 and funded under the Annual Development Plan of the Punjab Government or funded through foreign loans where the negotiations were finalized as on 1st of July 2016 or funded under Public Sector Development Program of the Federal Government or funded by Cantonment Boards.

Beauty parlors, salons, clinics, sliming clinics, spas

Services provided for personal care by beauty parlors, salons, clinics, sliming clinics, spas (including saunas, Turkish baths and Jacuzzi) and similar other establishments.

EXCLUDING: Services provided in a parlour, salon or clinic where the facility of air-conditioning is not installed or is not available in the premises on any day of the financial year.

Tax Rate: Five percent Without input tax adjustment where payment against Services is received through debit or credit cards; and Sixteen percent for others.

Information Technology enabled services and insurance claim Processing

Information technology-enabled or information technology based services including software development, software customization, software maintenance, system support, system assembly, system integration, system designing and architecture, system analysis, system development, system operation, system maintenance, system up-gradation and modification, data warehousing or management, data entry operations, data migration or transfer, system security or protection, web designing, web development, web hosting, network designing, services relating to enterprise resource or management planning (including marketing of products), development and sale of smart phone applications or games, graphics designing, medical transcription, remote monitoring, telemedicine, insurance claim Processing, online retrieval and database access or retrieval service.

Tax Rate: Five percent without input tax adjustment

Tour Operators & Travel agents

Services provided by tour operators and travel agents including all their allied services or facilities (other than Hajj and Umrah). Tax Rate: Five percent without input tax Adjustment

Manpower recruitment agent

Manpower recruitment agent including labour and manpower supplies. Tax Rate: (a) Five percent without input tax adjustment for services where the value of service is fixed by the Bureau of Emigration and Overseas Employment; and (b) Sixteen percent for others.

Property dealers and realtors

Services provided by property dealers and realtors. Tax Rate: Five percent without input tax adjustment.

Rent-a-car

Services provided in respect of rent-a-car (including renting of all categories of vehicles meant for transportation of persons). Tax Rate: (a) Five percent without input tax adjustment for services provided to end consumers; and (b) Sixteen percent for others.

Car / automobile dealers

Services provided by car/automobile dealers. Tax Rate: (a) Sixteen percent for services provided by companies or authorized dealers; and (b) Five percent without input tax adjustment, for others.

Processing on toll

Services provided in respect of manufacturing or processing on toll or job basis (against processing on conversion charges) including industrial and commercial packaging services and similar outsourcing of industrial or commercial processes. Tax Rate: Five percent without input tax adjustment

Commission agents

Brokerage (other than stock) and indenting services including commission agents, under-writers and auctioneers. Tax Rate: (a) Five percent without input tax adjustment for services provided in respect of agricultural produce; and (b) Sixteen percent for others.

Health care, gym, physical fitness

Services provided in specified fields such as health care, gym, physical fitness, indoor sports, games, amusement parks, arcades and other recreation facilities, and body or sauna massage etc. Tax Rate: Five percent without input tax adjustment

Cable TV operators

Services provided by cable TV operators. Tax Rate: Five percent without input tax adjustment

Accountants, auditors, actuaries, tax consultants

Services provided by accountants (including practicing chartered or cost accountants), auditors, actuaries, tax consultants (by whatever name called), practicing company secretaries, receivers, liquidators, auctioneers and corporate law consultants, whether individual or otherwise. Tax Rate: (a) Five percent without input tax adjustment for services relating to accountancy, audit, tax or corporate law consultancy; and (b) Sixteen percent for others.

By Air domestic and international travel

Facilities for travel originating from Punjab by Air for domestic and international travel. EXCLUDING: Air travel services provided to Hajj or Umrah passengers, diplomats and supernumerary crew. Tax Rate: Five percent without input tax adjustment.

Photographers / film-makers

Services provided by photography studios and event or occasion photographers/film-makers. EXCLUDING: Non-corporate (individual) photographers operating from small road-side shops declared as such by the Authority. Tax Rate: Five percent without input tax adjustment.

Skin and laser clinics

Services provided by skin and laser clinics, cosmetic and plastic surgeons and hair transplant services including consultation services. Excluding: Services provided to acid or burn victims. Tax Rate: Five percent without input tax adjustment.

Parking services

Parking services Tax Rate: Five percent without input tax adjustment.

Treatment of textile, leather

Services in respect of treatment of textile, leather but not limited to Dyeing services, Edging and cutting, cloth treating, water proofing, Embroidery, Engraving, Fabric bleaching, Knitting, Leather staining, Leather working, Pre-shrinking, Colour separation services, pattern printing and shoe making services. Tax Rate: Five percent without input tax adjustment.

Others Services

Apartment house management, real estate management and services of rent collection. Tax Rate: Five percent without input tax adjustment.

Medical consultation/ visit fee exceeding Rs.1,500 per consultation/ visit of doctors, medical practitioners and medical specialists. (ii) Bed/ room charges of hospitals exceeding Rs.6,000/- per day per bed / room. Tax Rate: Zero percent without input tax adjustment.

Ride-Hailing Services. Tax Rate: Four percent without input tax adjustment.

Source | Punjab Revenue Authority | PRA | Sales Tax Rates | Reduced Rate of Sales Tax |

LATEST POSTS

- Pakistan Budget 2026-27: Proposed Salary Tax Rates for Salaried Individuals

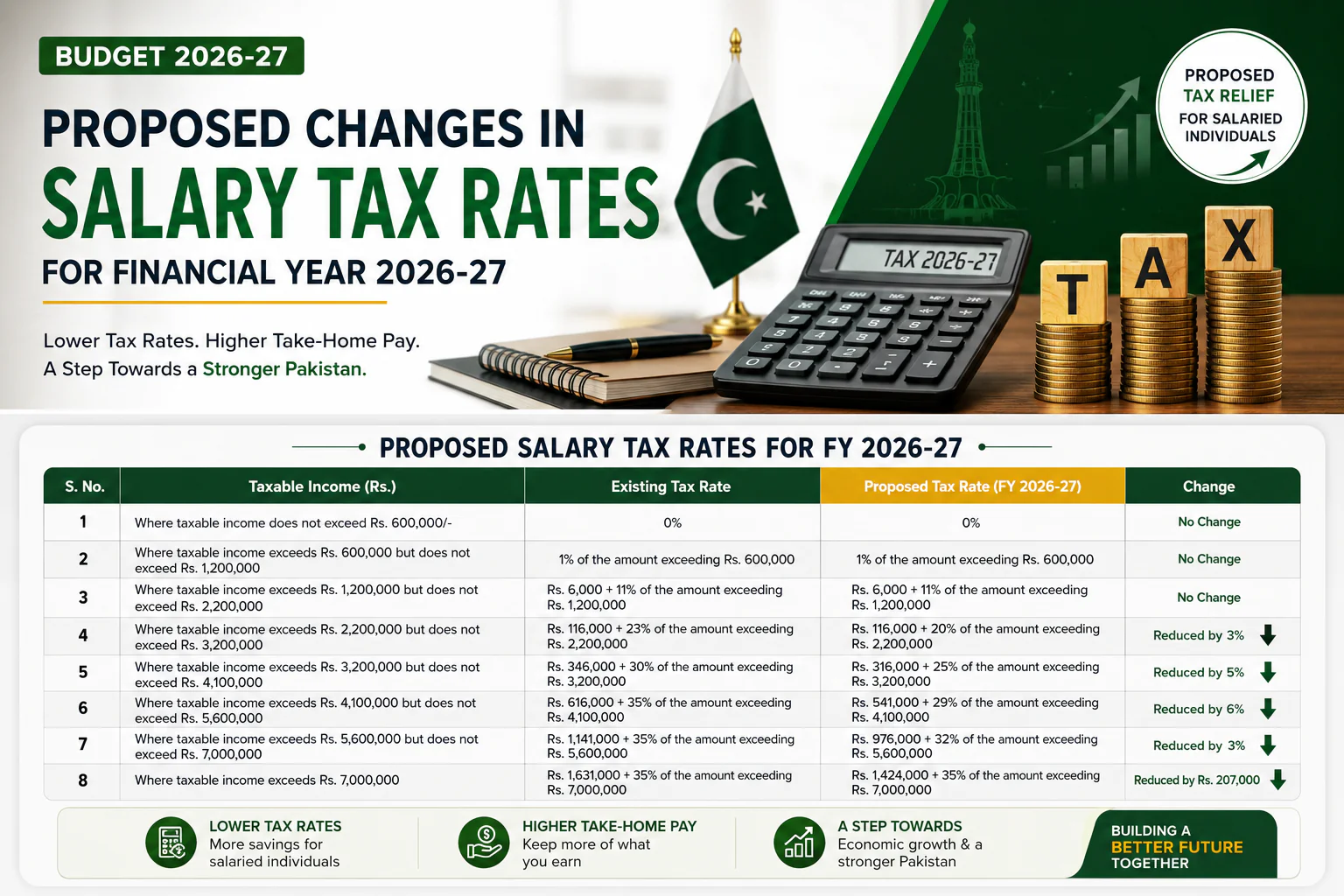

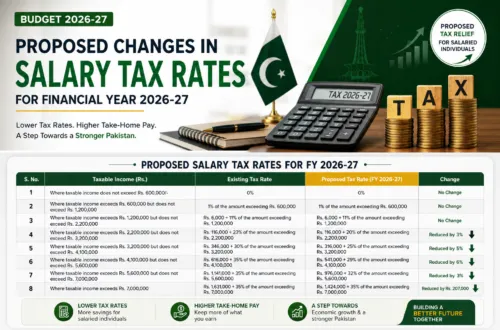

Proposed Salary Tax Rates for Salaried Individuals in Pakistan Budget 2026-27 The Finance Bill for the 2026‑27 budget proposes a reduction in income tax rates for salaried individuals. Most salaried taxpayers above Rs. 2.2 million in annual taxable income will enjoy a reduction in their tax liability. Here is the proposed slabs, existing salary tax rates, and how much salaried individuals can save once the changes in tax rates take effect. Proposed vs. Existing Salary Tax Rates for FY 2026‑27 S.No Taxable Income Existing Tax Rate Proposed Tax Rate 1 Up to Rs. 600,000 0% 0% 2 Rs. 600,000 – Rs. 1,200,000 1% of amount exceeding Rs. 600,000 1% of amount exceeding Rs. 600,000 3 Rs. 1,200,000 – Rs. 2,200,000 Rs. 6,000 + 11% of amount exceeding Rs. 1,200,000 Rs. 6,000 + 11% of amount exceeding Rs. 1,200,000 4 Rs. 2,200,000 – Rs. 3,200,000 Rs. 116,000 + 23% of amount exceeding Rs. 2,200,000 Rs. 116,000 + 20% of amount exceeding Rs. 2,200,000 5 Rs. 3,200,000 – Rs. 4,100,000 Rs. 346,000 + 30% of amount exceeding Rs. 3,200,000 Rs. 316,000 + 25% of amount exceeding Rs. 3,200,000 6 Rs. 4,100,000 – Rs. 5,600,000 Rs. 616,000 + 35% of amount exceeding Rs. 4,100,000 Rs. 541,000 + 29% of amount exceeding Rs. 4,100,000 7 Rs. 5,600,000 – Rs. 7,000,000 Rs. 1,141,000 + 35% of amount exceeding Rs. 5,600,000 Rs. 976,000 + 32% of amount exceeding Rs. 5,600,000 8 Above Rs. 7,000,000 Rs. 1,631,000 + 35% of amount exceeding Rs. 7,000,000 Rs. 1,424,000 + 35% of amount exceeding Rs. 7,000,000 Who Benefits the Most From the Proposed Salary Tax Slabs? The first two taxable slabs (income up to Rs. 2.2 million) are unchanged, means initial salaried tax slabs won’t see any difference. The change starts from slab 4 onward up to slab no 7. How to Calculate Your Tax Under the New Slabs To calculate your annual tax liability of salary income, you have to identify which slab your taxable salary income falls into. Then apply the formula for that slab: the fixed amount of salary tax plus the stated percentage of salary tax rate of that slab multiply by the income exceeding the slab’s lower threshold. For example, someone earning Rs. 4,500,000 falls in slab 6: Rs. 541,000 + 29% of (Rs. 4,500,000 − Rs. 4,100,000) = Rs. 541,000 + Rs. 116,000 = Rs. 657,000. Additional Tax Surcharge Removed Government of Pakistan has also proposed in the budget 2026-2027 removal of tax surcharge @9% on salary income if it is above than Rs 10 Million Rupees per annum. It is in addition to salary tax rates reductions proposed in the budget. FAQs Section TAGS A step-by-step guide to filing an income tax return | How to compute monthly withholding tax from salary | Budget 2026-27 | Salary Tax Slabs | Income Tax Rates | Finance Bill 2026-27 | Tax Calculator | Salaried Individuals Tax | Income Tax Ordinance | FBR Tax Slabs | Tax Relief | Withholding Tax | Salary Tax Rates 2026-27 | New Tax Slabs Pakistan | Income Tax Calculation Guide | Budget Tax Changes |

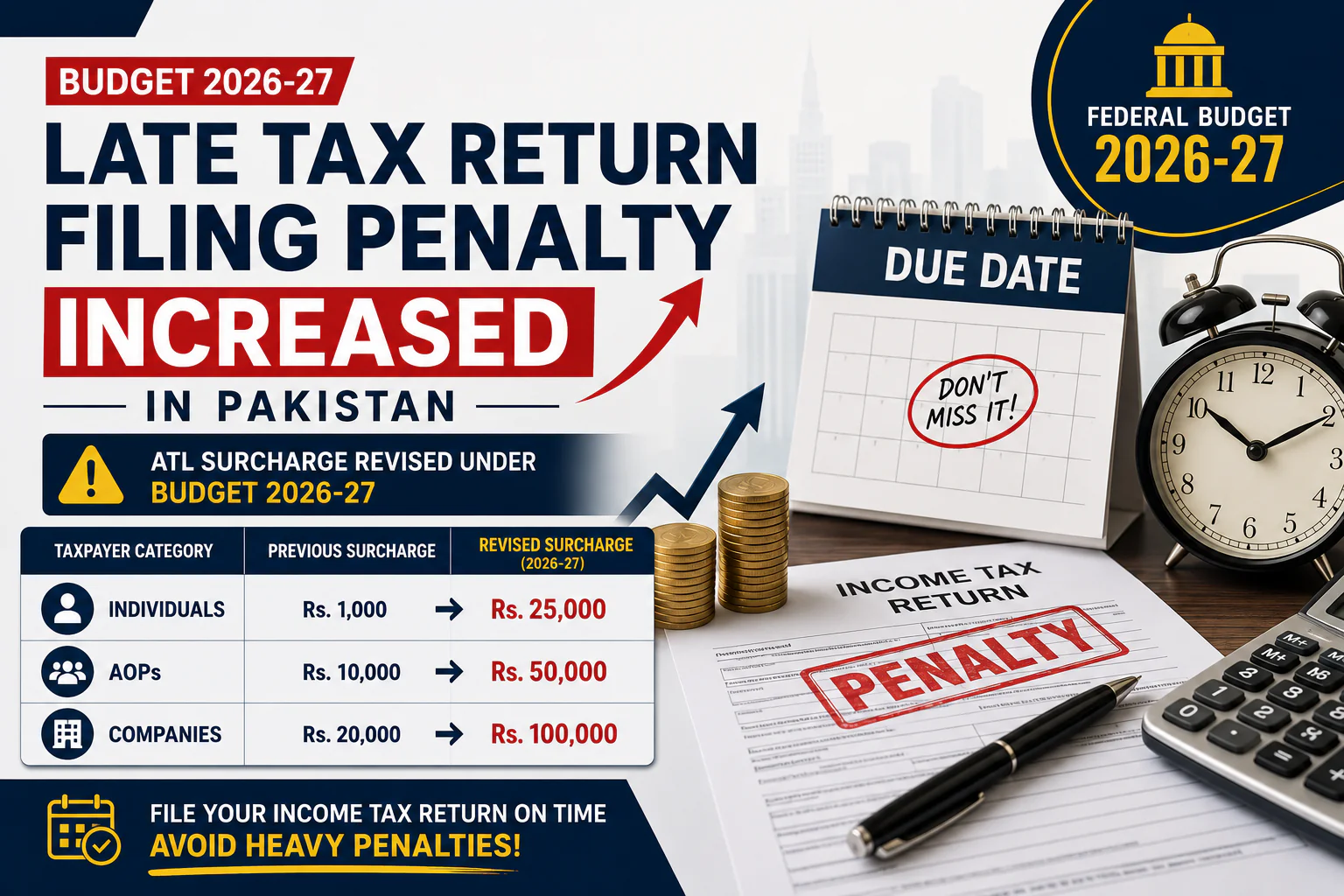

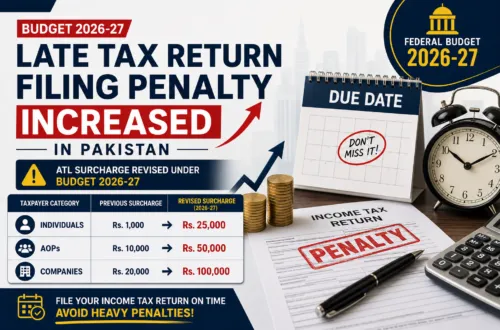

Proposed Salary Tax Rates for Salaried Individuals in Pakistan Budget 2026-27 The Finance Bill for the 2026‑27 budget proposes a reduction in income tax rates for salaried individuals. Most salaried taxpayers above Rs. 2.2 million in annual taxable income will enjoy a reduction in their tax liability. Here is the proposed slabs, existing salary tax rates, and how much salaried individuals can save once the changes in tax rates take effect. Proposed vs. Existing Salary Tax Rates for FY 2026‑27 S.No Taxable Income Existing Tax Rate Proposed Tax Rate 1 Up to Rs. 600,000 0% 0% 2 Rs. 600,000 – Rs. 1,200,000 1% of amount exceeding Rs. 600,000 1% of amount exceeding Rs. 600,000 3 Rs. 1,200,000 – Rs. 2,200,000 Rs. 6,000 + 11% of amount exceeding Rs. 1,200,000 Rs. 6,000 + 11% of amount exceeding Rs. 1,200,000 4 Rs. 2,200,000 – Rs. 3,200,000 Rs. 116,000 + 23% of amount exceeding Rs. 2,200,000 Rs. 116,000 + 20% of amount exceeding Rs. 2,200,000 5 Rs. 3,200,000 – Rs. 4,100,000 Rs. 346,000 + 30% of amount exceeding Rs. 3,200,000 Rs. 316,000 + 25% of amount exceeding Rs. 3,200,000 6 Rs. 4,100,000 – Rs. 5,600,000 Rs. 616,000 + 35% of amount exceeding Rs. 4,100,000 Rs. 541,000 + 29% of amount exceeding Rs. 4,100,000 7 Rs. 5,600,000 – Rs. 7,000,000 Rs. 1,141,000 + 35% of amount exceeding Rs. 5,600,000 Rs. 976,000 + 32% of amount exceeding Rs. 5,600,000 8 Above Rs. 7,000,000 Rs. 1,631,000 + 35% of amount exceeding Rs. 7,000,000 Rs. 1,424,000 + 35% of amount exceeding Rs. 7,000,000 Who Benefits the Most From the Proposed Salary Tax Slabs? The first two taxable slabs (income up to Rs. 2.2 million) are unchanged, means initial salaried tax slabs won’t see any difference. The change starts from slab 4 onward up to slab no 7. How to Calculate Your Tax Under the New Slabs To calculate your annual tax liability of salary income, you have to identify which slab your taxable salary income falls into. Then apply the formula for that slab: the fixed amount of salary tax plus the stated percentage of salary tax rate of that slab multiply by the income exceeding the slab’s lower threshold. For example, someone earning Rs. 4,500,000 falls in slab 6: Rs. 541,000 + 29% of (Rs. 4,500,000 − Rs. 4,100,000) = Rs. 541,000 + Rs. 116,000 = Rs. 657,000. Additional Tax Surcharge Removed Government of Pakistan has also proposed in the budget 2026-2027 removal of tax surcharge @9% on salary income if it is above than Rs 10 Million Rupees per annum. It is in addition to salary tax rates reductions proposed in the budget. FAQs Section TAGS A step-by-step guide to filing an income tax return | How to compute monthly withholding tax from salary | Budget 2026-27 | Salary Tax Slabs | Income Tax Rates | Finance Bill 2026-27 | Tax Calculator | Salaried Individuals Tax | Income Tax Ordinance | FBR Tax Slabs | Tax Relief | Withholding Tax | Salary Tax Rates 2026-27 | New Tax Slabs Pakistan | Income Tax Calculation Guide | Budget Tax Changes | - Budget 2026-27: Government Proposes Massive Increase in Late Tax Return Filing PenaltiesLate Tax Return Filing Penalty Increased in Pakistan Under Budget 2026-27 The Federal Budget 2026–27 has proposed a major increase in the late tax return filing penalties (ATL surcharge) imposed on taxpayers (individuals, AOPs and Companies) who file their income tax returns after the due date. Through an amendment to Section 182A(1)(a) of the Income Tax Ordinance, 2001, the Federal Government has revised the ATL (Active Taxpayers List) surcharge as follows: Taxpayer Category Previous Surcharge Proposed Surcharge Individuals Rs. 1,000 Rs. 25,000 AOPs Rs. 10,000 Rs. 50,000 Companies Rs. 20,000 Rs. 100,000 The proposed amendment is to encourage timely filing of income tax returns and increase tax compliance across the country. The increase is particularly significant for individuals, where the surcharge raised twenty-five times from Rs. 1,000 to Rs. 25,000. Similarly, companies may face a surcharge of Rs. 100,000 for late filing, compared to the previous amount of Rs. 20,000. Now, taxpayers are advised to file their annual income tax returns within the prescribed due dates to avoid heavy penalties and maintain their status on the Active Taxpayers List (ATL) with FBR. How to File Income Tax Return in Pakistan | Benefits of Being an Active Taxpayer | ATL Status Check Online | FBR Iris Registration Guide | Income Tax Return Due Dates in Pakistan | Penalties for Non-Filers in Pakistan | Budget 2026-27 Highlights | Income Tax Rates in Pakistan 2026

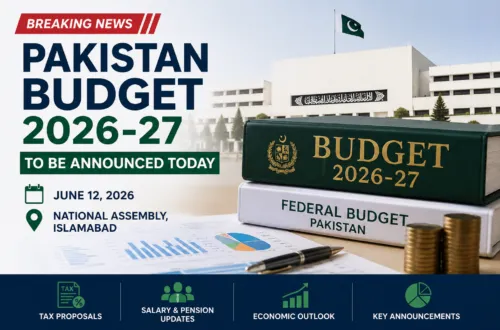

- Pakistan Budget 2026-27 to Be Presented Today in National AssemblyPakistan Budget 2026-27 to Be Announced Today Islamabad, June 12, 2026: The Federal Government is scheduled to present the Pakistan Budget 2026-27 in the National Assembly today. Finance Minister Muhammad Aurangzeb will present the federal budget proposals for the upcoming fiscal year 2026-2027. He will unveil it after approval by the Federal Cabinet. The National Assembly session for the budget presentation is expected to begin at 3:00 PM. The budget is expected on the government’s revenue targets, expenditure plans, taxation measures, and key economic priorities for FY 2026-27. Businesses, taxpayers, investors, and salaried individuals all over the Pakistan are keenly watching today’s budget announcement for any changes in taxes, salaries, pensions, and other fiscal measures. Tax.net.pk will provide live updates, budget highlights, and detailed analysis immediately after the budget speech. Tags Federal Budget Pakistan | Income Tax Rates in Pakistan | FBR Tax Updates | Salary Tax Calculator Pakistan | Withholding Tax Rates in Pakistan | Prize Bond Draw Schedule 2026 | Petrol Prices in Pakistan | Pakistan Economic Updates | Tax News Pakistan | Budget 2026-27 Highlights

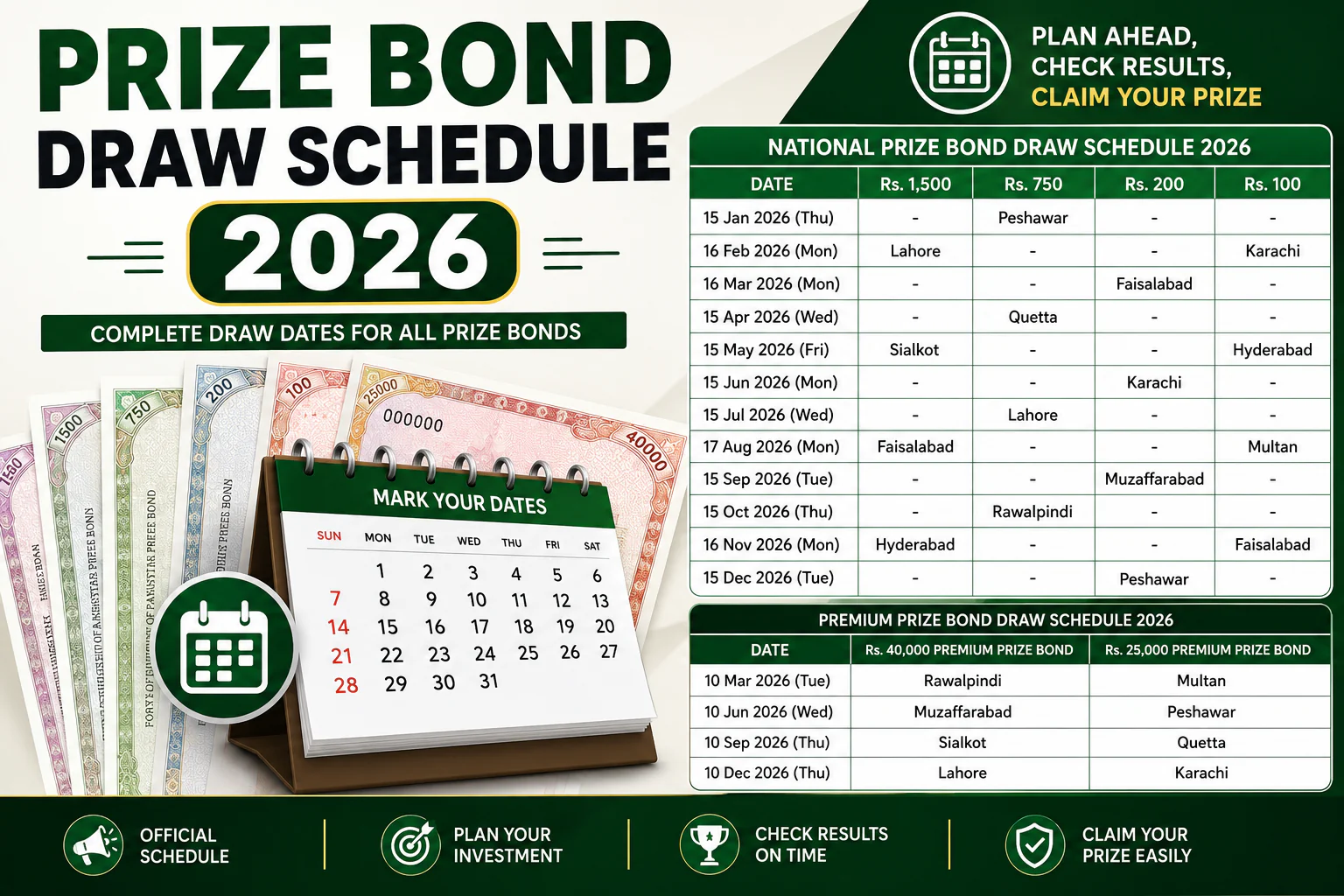

- Prize Bond Draw Schedule 2026 Pakistan – Complete Draw Dates ListPrize Bond Draw Schedule 2026 In Pakistan, prize bonds is very popular investment among the people. People like to invest in this mode of investment because it’s easy to invest, encash, backed by the Government of Pakistan, and profit is also paid on the premium prize bonds. Knowing prize bonds draw dates in advance is very important because you never miss a draw result, stay updated with official announcements, easy to manage, and timely prize money process, peace of mind. Here schedule for the year starting from January 2026 to December 2026 is given. Such schedule is for denominations of: Prize bond schedule for 2026 is also given here for premium prize bonds of: Prize Bond Draw Schedule 2026 Here prize bond draw schedule for 2026 is given for regular type of prize bonds which is not issued in name of investor. Any body can purchase it and invest easily. Schedule is for prize bonds for denominations of Rs 1500, Rs 750, Rs 200, and Rs 100. Date Rs. 1,500 Rs. 750 Rs. 200 Rs. 100 15 January 2026 (Thursday) – Peshawar – – 16 February 2026 (Monday) Lahore – – Karachi 16 March 2026 (Monday) – – Faisalabad – 15 April 2026 (Wednesday) – Quetta – – 15 May 2026 (Friday) Sialkot – – Hyderabad 15 June 2026 (Monday) – – Karachi – 15 July 2026 (Wednesday) – Lahore – – 17 August 2026 (Monday) Faisalabad – – Multan 15 September 2026 (Tuesday) – – Muzaffarabad – 15 October 2026 (Thursday) – Rawalpindi – – 16 November 2026 (Monday) Hyderabad – – Faisalabad 15 December 2026 (Tuesday) – – Peshawar – Premium Prize Bond Draw Schedule 2026 This premium prize bonds schedule is for denominations of Rs 40,000 and Rs 25,000. Draw of premium prize bonds is held quarterly. This type of prize bond is issued in the name of investor. It has benefits like, it is very secure, no risk of theft, profit on investment, and easy to manage. Draw of Premium prize bonds is held quarterly in the following months: Date Rs. 40,000 Premium Prize Bond Rs. 25,000 Premium Prize Bond 10 March 2026 (Tuesday) Rawalpindi Multan 10 June 2026 (Wednesday) Muzaffarabad Peshawar 10 September 2026 (Thursday) Sialkot Quetta 10 December 2026 (Thursday) Lahore Karachi How to Check Latest Prize Bonds Draw Result Online Prize Bond List Online check through: Call to Action If you need help with NTN registration, income tax return filing, ATL status, or FBR matters? You may please Contact Global Tax Consultants for professional tax advisory and compliance services across Pakistan. 💬 WhatsApp Chat 📞 Call Now

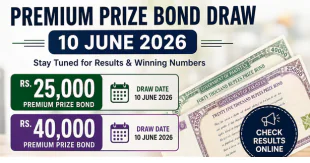

- Premium Prize Bond Draw 10 June 2026 for Rs. 25,000 and Rs. 40,000 BondsPremium Prize Bond Draw for Rs. 25,000 and Rs. 40,000 on 10 June 2026 The next Premium Prize Bond Draw for denominations of Rs. 25,000 and Rs. 40,000 is scheduled to be held on 10 June 2026. Prize bond holders across Pakistan wait for the official draw results announced by the State Bank of Pakistan (SBP) and National Savings Pakistan. Premium Prize Bonds is very popular among public because: they offer regular profit payments and opportunity to win prizes as well. What Are Premium Prize Bonds? Premium Prize Bonds are different from regular prize bonds, these bonds provide: Currently, Premium Prize Bonds are available in denominations of Rs. 25,000 and Rs. 40,000. Next Draw Date and Details Premium Prize Bond Rs. 25,000 Draw Premium Prize Bond Rs. 40,000 Draw The official winning numbers will be announced after the draw is conducted by National Savings Pakistan. How to Check Premium Prize Bond Draw Results Online Prize bond holders can check the draw results through: After the draw, winning lists will be available for online verification. Benefits of Investing in Premium Prize Bonds Premium Prize Bonds offer many benefits: Regular Profit Income Premium bond holders receive profit payments directly into their linked bank accounts. Chance to Win Prizes In addition to profit income, investors can also win prize amount on scheduled draw dates. Government-Backed Investment Premium Prize Bonds are issued by the Government of Pakistan, making them one of the reliable investment options. Easy to Maintain and No Risk of Theft Premium bonds are registered in the investor’s name, ownership records remain secure and no risk of theft. When Will the Result Be Available? The official draw result is announced after the draw will be held on 10 June 2026. Once announced, bond holders can search their bond numbers online and verify whether they have won any prize. Stay Updated If you hold Premium Prize Bonds of Rs. 25,000 or Rs. 40,000, make sure to check back on 10 June 2026 for the latest draw results, winning numbers, and prize details. We will update this page immediately after the official announcement.

- New Taxes on E-commerce Transactions in PakistanNew Taxes on E-commerce Transactions in Pakistan: In the recent budget (Finance Act 2025) Government of Pakistan has taken some significant steps towards the taxation of local ecommerce industry of Pakistan. The new amendments in the Income tax Ordinance 2001 and Sales Tax Act 1990 will affect all those ecommerce businesses operating through online platforms, websites, or courier based Cash on Delivery (COD) Model. Below are the significant highlights of amendments in tax laws of Pakistan which are necessary for your understanding: Enhanced Definition of “Online Market Place” Through Finance Act 2025, section 2(38B) of income Tax Ordinance 2001 amended and definition of “Online Market Place” has been broadened. It now also includes: These will help buying and selling between multiple parties, whether the platform owns the goods/services or not. New Taxes on E-commerce Transactions in Pakistan for Digitally Ordered Goods/Services Through Finance Act 2025, a new section, 6A in the Income Tax Ordinance, introduces a tax on payments received for digitally ordered goods/services through local platforms (including websites). Applies To:This section applies to all persons receiving payments for goods/services delivered from within Pakistan via online platforms. Excludes:It does not include export proceeds received in Pakistan which are already taxed under sections 154 and 154A. Tax Collection by Payment Intermediaries and & Couriers Under amendment in section 153(2A) of Income Tax Ordinance 2001 through Finance Act 2025: This applies to all payments made for digitally ordered goods and services via local platforms, including websites. Rate of Income tax to be deducted from a payment for digitally ordered goods/services Two different tax rates has been introduced for payments to ecommerce sellers against digitally ordered goods, complete description is here: Sales Tax Collection Responsibility As per Sales Tax Act 1990, the responsibility to collect and pay sales tax on digitally ordered goods is explained here: Rates of Sales Tax on Payments against Digitally ordered goods The applicable rates of sales tax to be deducted are given in the Eleventh Schedule of the Sales Tax Act 1990. The sales tax withheld by the payment intermediary or the courier company will be final discharge of tax liability against the digitally ordered goods by the: AS per the eleventh schedule of Sales Tax Act 1990 the rate of sales tax to withhold to withhold by the payment intermediary / Courier Company will be at the rate of 2% of gross value of supplies. Mandatory NTN & Sales Tax Registration To promote documentation and transparency: Unregistered sellers will not be allowed to operate on their platforms.

TaxUrdu.com

One comment on “Sales Tax Relief by Punjab Revenue Authority”

Comments are closed.